Easterly Government Properties ($DEA)

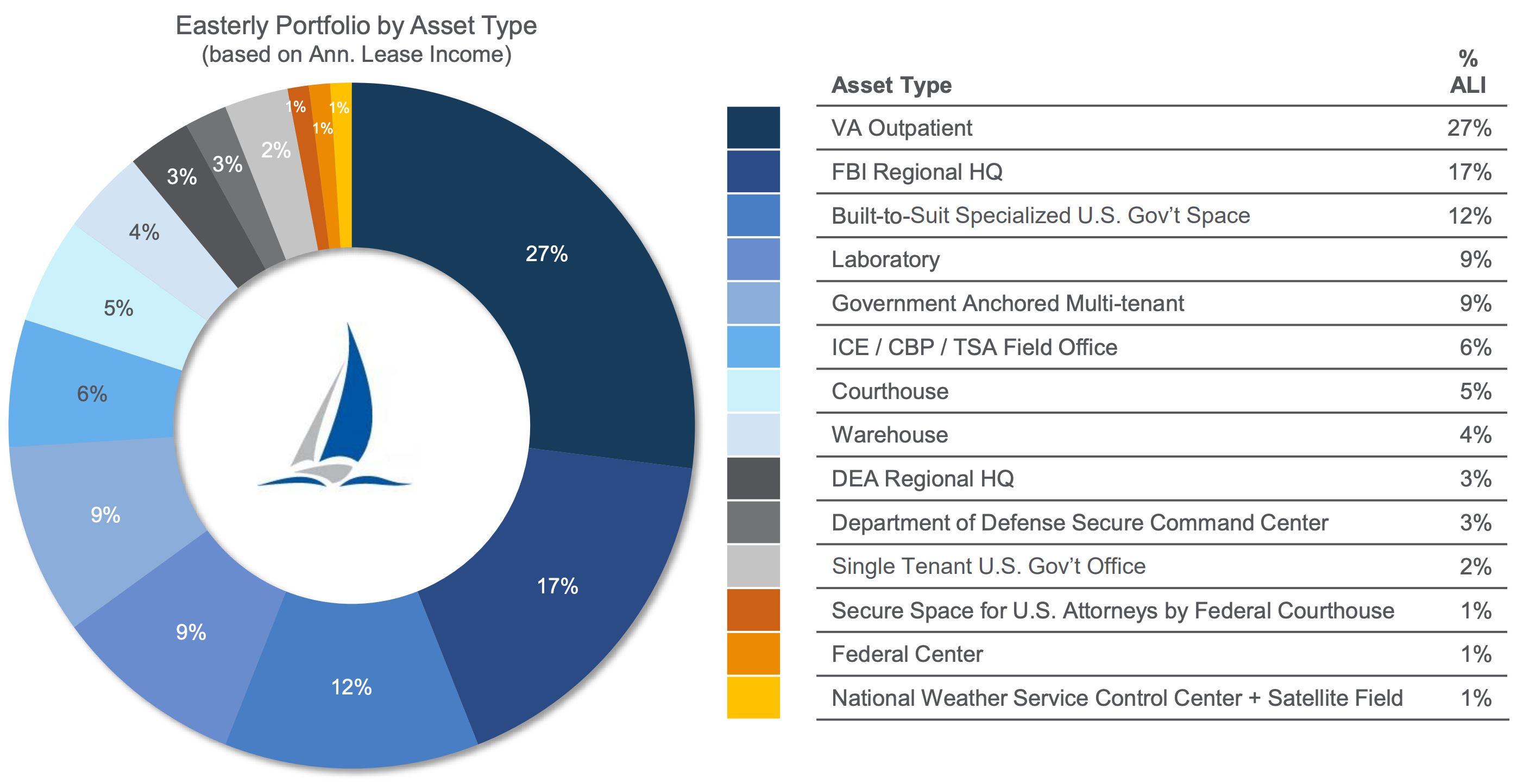

Easterly Government Properties is a REIT that primarily leases properties to “critical” departments of the US federal government, though they recently began diversifying into state and local governments and stable private sector tenants. Currently they claim that 93% of lease income is backed by the full faith and credit of the U.S. government. As of March 2025, the weighted average firm lease term was 8.6 years.

Despite the recession-proof tenants on long leases, the stock trades at a P/FFO of 6.7. The stock is down 45% from its 52 week high, in large part due to fears relating to DOGE’s campaign to cut government waste. However, I believe these fears are very overblown and it actually seems more likely that the impact of DOGE will be bullish rather than bearish.

While it’s true that DOGE is terminating many federal leases, 643 as of today, and will likely continue to terminate more, most of Easterly’s properties should be safe because they are properties that are actually being utilized for important government functions.

I have only managed to find reporting of one Easterly property that was terminated, and DOGE said its value was $1M, which is a tiny fraction of Easterly’s $323M annual lease income. Today, the CEO said in the 2025 Q1 earnings call, “To date, we have not had a single lease canceled due to DOGE.”

As of March 17th, an analysis by CoStar found just 13 of the 800 DOGE lease terminations at that time affected the 11,500 properties owned by 11 publicly traded REITs. Given that the article mentions Easterly explicitly, it should be safe to assume that Easterly’s terminations are a subset of those 13. This is despite the fact that as of March 3rd, DOGE had already cancelled about 10% of federal leases.

Note that when DOGE “terminates” a lease, they are not breaking the lease contract, they are just exercising an option to cancel after the “firm” period of the lease is over. So the 8.6 year weighted average firm lease term is not susceptible to DOGE terminations.

I think some people are getting confused by anti-DOGE propaganda that is making it sound like they are slashing huge portions of the government, when in reality they are mostly looking for low-hanging fruit in the form of blatant waste and fraud.

Easterly’s CEO Darrell Crate is a Republican and former chair of the Massachusetts Republican Party. I think he and the company are largely aligned with the current administration in regards to which parts of the federal government are necessary vs. unnecessary, and this is reflected in Easterly’s property portfolio.

On the other hand, there are several reasons why DOGE could actually be bullish for Easterly:

Trump issued an executive order ending remote work for the executive branch, which increases demand for office space.

Trump wants federal agencies to move offices out of D.C. to less costly areas. Easterly only has 7% of lease income in the national capital region and all of that is in Virginia and Maryland as of December 31st, 2024, though they did acquire one property in D.C. at a 9% cap rate in 2025 Q1. This should generate growth opportunities for Easterly since they develop properties for the government in these cheaper areas.

Easterly’s CEO believes that leasing is more cost-effective than owning for the government and claims that Easterly can build for 1/3 the price that it would cost the government.

Even if lease terminations do turn out to be a serious headwind, these considerations might cancel out or at least blunt the impact. But I think the way to think about this is that the current administration is focused on reducing waste while Easterly is already positioned with a low waste portfolio.

On April 9th, the stock plunged from already low levels due to a large dividend cut. Some investors likely saw this as confirmation of their fears regarding DOGE, but I don’t think that’s the case. The real reason is that the company was using share issuance to partially fund growth and the dividend. In the 2024 Q4 earnings call, the CEO said “if the stock was at $13 [before 1-for-2.5 reverse split] covering the dividend is no problem.” So basically, DOGE fears pushed the stock price down to a point where they could no longer utilize share issuance as a funding source, which forced them to cut the dividend. Ideally they wouldn’t have been relying on share issuance in the first place, but at least now they won’t have to anymore. As further evidence, the company just raised their 2025 FFO guidance slightly today.

The real headwind in my mind is rising interest rates on their debt, just as with most REITs. They have $1.6B in net debt at an interest rate of 4.6% and a weighted average maturity of 4.8 years. With the 10 year treasury currently at around 4.2%, they aren’t going to be able to roll their debts at the same rates. On March 25, 2025 they issued senior unsecured debt at 6.13% and 6.33%. If we assume that all their debt is rolled at 6.2%, the interest expense will increase from $74M to $99M, an increase of $25M/year. If we subtract this from the FFO guidance, it would reduce FFO/share from $3.00 to $2.44, neglecting tax savings. Note that we are probably being a bit conservative here because this number is based on unsecured debt so they do have cheaper funding sources available.

So let’s consider a scenario that I would view as somewhat conservative where DOGE cancels out all of the targeted 2.5% growth and the weighted average interest rate rises to 6.2% over the next few years. Then we’d have $2.44/sh FFO with both the DOGE and interest rate headwinds resolved and a 2.5% growth rate resuming. In that situation I think it should get at least a 12x P/FFO ratio, if not higher, which would be $29.28/sh. But during the initial years the interest rate is lower, so there is some additional benefit, so let’s just round to $30. I think that’s a conservative fair value today. For comparison, Tikr has the median analyst NAV at $35, which is probably a reasonable fair value if you aren’t being conservative.

So at $20, DEA has 50% upside to conservative fair value and pays a well-covered 9% dividend. Plus it is one of the most recession-proof stocks you can find and should even benefit from a recession if interest rates are lowered. So it is one of the very rare stocks that has counter-cyclical tendencies similar to treasury bonds, though of course it does have some non-cyclical risks. Because I’m not that worried about DOGE, my main concern is that they might dilute the undervaluation away with continued share issuance. But with the large dividend cut, they shouldn’t have to and hopefully they will be smart enough not to. In the 2025 Q1 earnings call, the CEO said “we don't have to access the equity markets in order to accomplish what we are intending to accomplish. We would issue equity if we can do that on an accretive basis.” An unexpected large rise in interest rates is another risk, but there are many cheap cyclical stocks available to help hedge that risk. I don’t consider the size of the debt to be a major risk unless we see lots of lease terminations and/or non-renewals. The debt was rated BBB as of March 26th, 2025, which is investment grade.