Golar LNG Update ($GLNG)

Golar was introduced in this post.

Although Golar achieved a 79% total return since my original post last March, I believe that it is just as bullish today as it was then and I’m still adding more shares despite it being by far my biggest position.

I think the market is being understandably conservative in pricing GLNG because there is still a lot of uncertainty:

We still don’t know the terms of the commodity-linked tariff of the new Hilli contract with PAE, which is definitive but is not yet FID.

The commodity-linked tariff depends on future LNG prices which are difficult to predict with confidence.

We don’t know for sure whether the newbuild MkII will get contracted.

We don’t know if Golar will exercise its option to build a second MkII and wether that vessel will get contracted.

However, we can get a sense of the likelihoods of these factors which will help us get a sense of where the valuation will end up.

Valuation

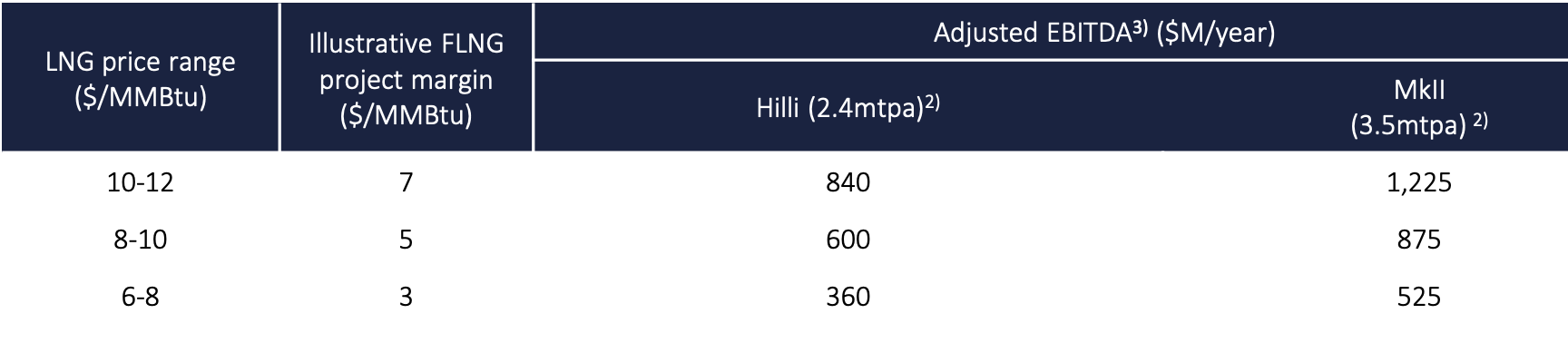

To get valuation estimates of Golar, we will have to make some big assumptions about the commodity-linked tariffs. Analysts seem to have fixed on a commodity-linked contribution of 20% of the base tariff, but this is quite low compared to the direct evidence that we have.

In the Golar 2023 Q4 Results Presentation, this chart was presented with a mid-range “illustrative” commodity-linked contribution of 100% of the base tariff, with the analysts’ 20% being the low-end example.

It’s important to consider that these “illustrative” terms may be aspirational and could get negotiated down in the actual contracts. I would assume that it is much more likely these numbers get negotiated down than up since this is what Golar is aiming for and likely the starting point of negotiations.

Also, this chart has been removed from more recent presentations and Golar has seemed to de-emphasize the commodity-linked tariff e.g. “Each MKII unit has potential to add ~$0.5BN of Annual Adjusted EBITDA based on the terms of the recently announced Argentina contract.” However, this is in the context of a slide about EBITDA backlog, and of course commodity-linked tariffs would not be considered part of backlog. I think this is why analysts are fixing on a 20% commodity-linked tariff contribution.

However, the terms of the current Hilli contract have a commodity-linked tariff that works out to be approximately equal to the base tariff, which is consistent with the 100% factor of the mid-range illustrative guidance.

I will use the “illustrative” terms in the chart above for the valuation matrix, with the caveat that these are based on potentially aspirational assumptions.

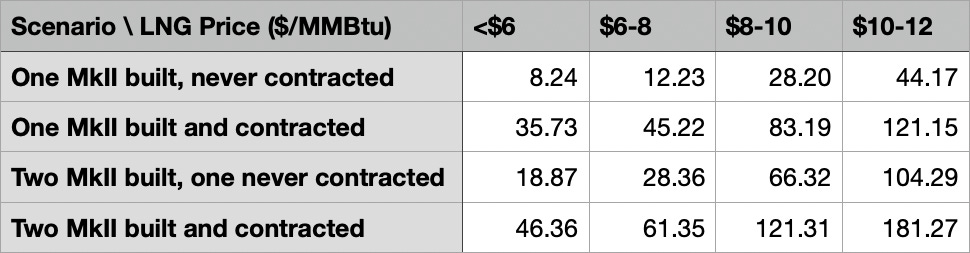

Clearly there is a wide range of outcomes, but as I discussed in the previous post, I think it is very unlikely that one of these vessels gets built and never gets contracted, so the first and third rows are very low probability scenarios.

As we discuss below, we will probably be in either the second of fourth scenario by the end of the year.

Also, keep in mind that longer-term there could be even more bullish scenarios involving more than two additional contracts.

LNG Prices

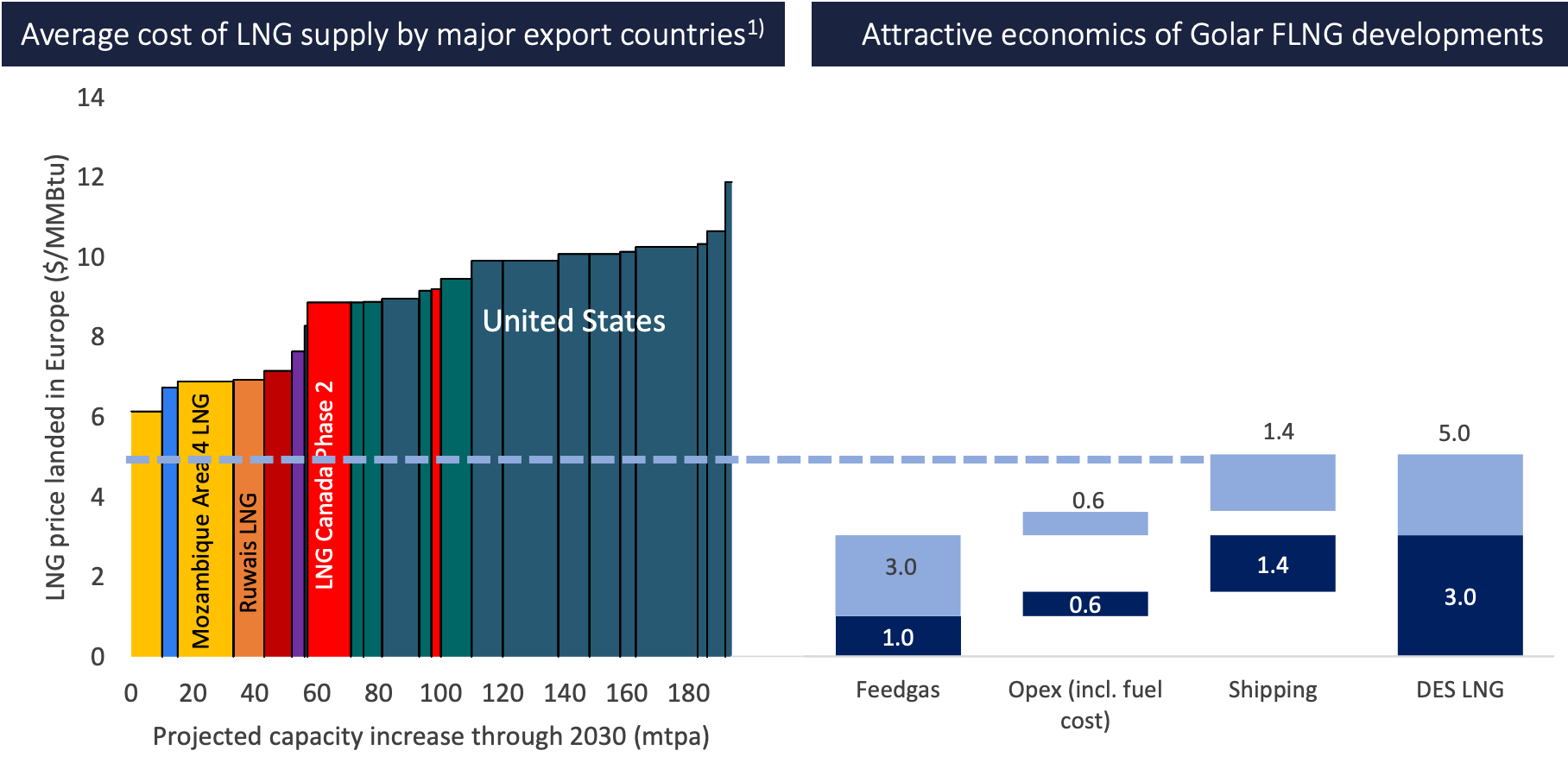

The valuation matrix shows how much the valuation depends on future LNG prices. The evidence seems to support Golar’s middle range of $8-10/MMBtu.

Current LNG prices are actually higher than the high end range at $14/MMBtu, but there is a widespread expectation that prices will come down due to the arrival of new supply. (Europe LNG Futures) (Europe LNG Price Chart) (Asia LNG Price Chart)

A year ago, one analyst said “over the next 3 years [LNG prices] could fall from $15/MMBtu to $8-$9/MMBtu“ (S&P Global Commodity Insights Jan 19, 2024).

A few days ago, an Argentinian Cabinet Minister tweeted a figure that implied a long-term LNG price of $9/MMBtu after discussions with Golar partner YPF, which suggests that Golar’s counterparties have similar expectations.

This $9/MMBtu target is based on a cost curve analysis that accounts for all of the new supply coming online in the near future. Golar presented this chart in their 2023 Q4 Results Presentation.

So I think that the mid-range of $8-10/MMBtu seems like the most likely scenario and upside and downside risks from there should be roughly balanced.

Contracts

It is very important that Golar gets a contract for it’s MkII newbuild. Fortunately it seems like there is a very good chance that they will get one soon.

Last year it sounded like they were going to get a contract with Nigeria, but that deal may have fallen through or maybe it’s just delayed. Management didn’t really explain what happened, but they said in the 2024 Q3 earnings call, “I don't think they're having right now a project that's suitable for the FLNGs available… but they are one of the contenders when we say that we think we'll have the unit contracted within 2025.”

The main contender now seems to be YPF, who recently joined the joint venture between Golar and PAE that is leasing the Hilli, where they have “committed to supplying 16.7% of the natural gas volumes to the project.”

The story with YPF is a bit complicated. They were originally planning on working with Petronas, but on December 19, 2024 it was reported that YPF had signed a contract with Shell and “Petronas' participation in the project had ended.” (Reuters)

Initially it sounded like YPF and Shell were going to build two new 5 mtpa FLNGs for the project.

Phase 1 of the project will include two floating liquefaction units located near the shore, each with a capacity of 5 mtpa. Next, Phase 2 envisages the construction of a 10-mtpa onshore modular liquefaction plant, which is set to be expanded by adding two trains as part of Phase 3. The final capacity is expected to reach up to 30 mtpa.

Offshore Energy January 22, 2025

Note that the Golar MkII is only 3.5 mtpa, so this sounded like it would exclude the possibility of leasing the Golar MkII. Although Golar does have an MkIII design that could be over 5 mtpa, they don’t seem to be focused on that at all.

However, it was recently reported that YPF changed their plans and is now considering deploying 4 FLNGs including potentially a second Golar vessel.

The LNG export project is advancing faster than had been expected. In December, Shell agreed to join Argentina LNG with the aim of building an initial 10 million mt/year of production capacity.

The project initially called for installing two floating liquefaction terminals and an onshore facility in the San Matías Gulf, a deep-water bay in Río Negro province due east of Vaca Muerta. But YPF is now considering installing a cluster of four FLNGs, of which the first has been ordered by BP-backed Pan American Energy, or PAE, from Norways' Golar LNG, a $3 billion project. The Hilli Episeyo FLNG will have capacity to produce 2.45 million mt/year of LNG, or 11.5 million cu m/d of gas, starting in the second half of 2027.

YPF has said it could order a second FLNG from Golar or another supplier to install alongside PAE's. The second FLNG will have more capacity -- at around 3.6 million mt/year -- and be installed to start operations at the end of 2027 or early 2028, while the others will follow by as soon as 2028, the source added.

S&P Global Commodity Insights January 21, 2025

It seems that YPF realized that Golar can provide vessels sooner and at lower cost than any other option. As discussed in the previous post, Shell built the world’s first large-scale FLNG vessel, but struggled with many operational issues, has higher costs than Golar, and it is still Shell’s only FLNG.

I am guessing that YPF wants a large partner like Shell, but as they discover that Golar is an economically superior partner for FLNG, I expect YPF to be more inclined to deal with Golar.

Additionally, there was recently a hint that the FLNGs would be operated by a “consortium.”

The company closed trade agreements in Asia for up to 15 million tons of liquefied natural gas (LNG) per year, which would represent more than 7,000 million dollars annually in exports to the country.

In parallel, Minister Francos anticipated that new sales contracts with European energy companies will be announced in the coming weeks, that could add up to an additional 4 million tons to the volume already committed.

In addition, liquefaction ships managed by a consortium of the main companies in the sector will be installed.

Adnsur January 28, 2025

It seems like there is a good chance that this “consortium” refers to the Golar-PAE-YPF consortium.

Additionally, although I consider this just a rumor because I can’t find a legitimate source, one investor tweeted that YPF already announced a contract with Golar.

YPF Fireside chat hosted by JPM. . . Finance officer just said they HAVE charted a vessel from GLNG with tolling arrangements (This is the Fuji).

KC Ambrecht December 13, 2024

Given all of this, it seems like YPF is anxious to ramp up exports and they have realized that Golar is going to be both the fastest and cheapest option, so I think there is a strong chance that we’ll see at least one contract with YPF this year.

There is also a chance that YPF contracts a second MkII with Golar, and Golar already has a yard option to build a second MkII. This would bring us to the last row in the valuation matrix, which is very bullish. If YPF used Golar for all of the 10 mtpa of the first phase, that would take 3 MkIIs, which would go beyond the most bullish scenario in the valuation matrix.

Also, regardless of what happens with YPF, I still think there’s a decent chance that the Nigeria deal happens eventually, and there are several other potential deals that Golar is discussing.

If just a few MkII deals work out, Golar should have a massive amount of upside.